Global sales of passenger cars were sluggish in 2019, but electric cars had another banner year

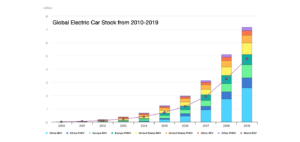

Sales of electric cars topped 2.1 million globally in 2019, surpassing 2018 – already a record year – to boost the stock to 7.2 million electric cars.1 Electric cars, which accounted for 2.6% of global car sales and about 1% of global car stock in 2019, registered a 40% year-on-year increase. As technological progress in the electrification of two/three-wheelers, buses, and trucks advances and the market for them grows, electric vehicles are expanding significantly. Ambitious policy announcements have been critical in stimulating the electric-vehicle rollout in major vehicle markets in recent years. In 2019, indications of a continuing shift from direct subsidies to policy approaches that rely more on regulatory and other structural measures – including zero-emission vehicles mandates and fuel economy standards – have set clear, long-term signals to the auto industry and consumers that support the transition in an economically sustainable manner for governments.

After entering commercial markets in the first half of the decade, electric car sales have soared. Only about 17 000 electric cars were on the world’s roads in 2010. By 2019, that number had swelled to 7.2 million, 47% of which were in The People’s Republic of China (“China”). Nine countries had more than 100 000 electric cars on the road. At least 20 countries reached market shares above 1%.2

The 2.1 million electric car sales in 2019 represent a 6% growth from the previous year, down from year-on-year sales growth at least above 30% since 2016. Three underlying reasons explain this trend:

Car markets contracted. Total passenger car sales volumes were depressed in 2019 in many key countries. In the 2010s, fast-growing markets such as China and India for all types of vehicles had lower sales in 2019 than in 2018. Against this backdrop of sluggish sales in 2019, the 2.6% market share of electric cars in worldwide car sales constitutes a record. In particular, China (at 4.9%) and Europe (at 3.5%) achieved new records in electric vehicle market share in 2019.

Purchase subsidies were reduced in key markets. China cut electric car purchase subsidies by about half in 2019 (as part of a gradual phase out of direct incentives set out in 2016). The US federal tax credit programme ran out for key electric vehicle automakers such as General Motors and Tesla (the tax credit is applicable up to a 200 000 sales cap per automaker). These actions contributed to a significant drop in electric car sales in China in the second half of 2019, and a 10% drop in the United States over the year. With 90% of global electric car sales concentrated in China, Europe and the United States, this affected global sales and overshadowed the notable 50% sales increase in Europe in 2019, thus slowing the growth trend.

Consumer expectations of further technology improvements and new models. Today’s consumer profile in the electric car market is evolving from early adopters and technophile purchasers to mass adoption. Significant improvements in technology and a wider variety of electric car models on offer have stimulated consumer purchase decisions. The 2018-19 versions of some common electric car models display a battery energy density that is 20-100% higher than were their counterparts in 2012. Further, battery costs have decreased by more than 85% since 2010. The delivery of new mass-market models such as the Tesla Model 3 caused a spike in sales in 2018 in key markets such as the United States. Automakers have announced a diversified menu of electric cars, many of which are expected in 2020 or 2021. For the next five years, automakers have announced plans to release another 200 new electric car models, many of which are in the popular sport utility vehicle market segment. As improvements in technical performance and cost reductions continue, consumers are placed in the position of being attracted to a product but wondering if it would be wise to wait for the “latest and greatest model”.

The Covid-19 pandemic will affect global electric vehicle markets, although to a lesser extent than it will the overall passenger car market. Based on car sales data during January to April 2020, our current estimate is that the passenger car market will contract by 15% over the year relative to 2019, while electric sales for passenger and commercial light-duty vehicles will remain broadly at 2019 levels. Second waves of the pandemic and slower-than-expected economic recovery could lead to different outcomes, as well as to strategies for automakers to cope with regulatory standards. Overall, we estimate that electric car sales will account for about 3% of global car sales in 2020. This outlook is underpinned by supporting policies, particularly in China and Europe. Both markets have national and local subsidy schemes in place – China recently extended its subsidy scheme until 2022. China and Europe also recently strengthened and extended their New Energy Vehicle mandate and CO2 emissions standards, respectively. Finally, there are signals that recovery measures to tackle the Covid-19 crisis will continue to focus on vehicle efficiency in general and electrification in particular.

Most charging is done at home and work, yet deploying publicly accessible charging points is outpacing electric vehicle sales

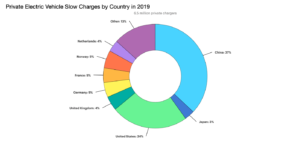

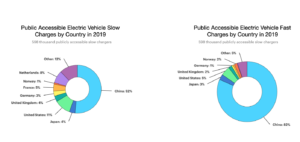

The infrastructure for electric-vehicle charging continues to expand. In 2019, there were about 7.3 million chargers worldwide, of which about 6.5 million were private, light-duty vehicle slow chargers in homes, multi-dwelling buildings and workplaces. Convenience, cost-effectiveness and a variety of support policies (such as preferential rates, equipment purchase incentives, and rebates) are the main drivers for the prevalence of private charging.

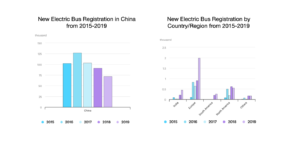

China continues to lead in electrifying two/three- wheelers and urban buses

Publicly accessible chargers accounted for 12% of global light-duty vehicle chargers in 2019, most of which are slow chargers. Globally, the number of publicly accessible chargers (slow and fast) increased by 60% in 2019 compared with the previous year, higher than the electric light-duty vehicle stock growth. China continues to lead in the rollout of publicly accessible chargers, particularly fast chargers, which are suited to its dense urban areas with less opportunity for private charging at home.

Transport modes other than cars are also electrifying. Electric micro-mobility options have expanded rapidly since their emergence in 2017, with shared electric scooters (e-scooters), electric-assist bicycles (e-bikes) and electric mopeds now available in over 600 cities across more than 50 countries worldwide. An estimated stock of 350 million electric two/three-wheelers, the majority of which are in China, make up 25% of all two/three-wheelers in circulation worldwide, driven by bans in many Chinese cities on two-wheelers with internal combustion engines. About 380 000 light commercial electric vehicles are in circulation, often as part of a company or public authority vehicle fleet.